This article is co-written by Fernando Da Cruz Vasconcellos, Ph.D. and Lucy Zhou, CPA.

Silicon Valley Bank, or SVB as it was commonly known, failed last Friday, 10 March 2023, sending shockwaves from Silicon Valley to Wall Street and around the world. Silicon Valley Bank had recently re-branded itself under the SVB platform in 2022.

This was the second biggest bank collapse in US banking history after Washington Mutual filed for bankruptcy and failed during the last financial crisis in 2008, 15 years ago. SVB was the 16th largest commercial bank in the United States. Unlike other similar commercial banks of its size (such as Huntington Bancshares), with over one thousand branches, SVB had only about 18 branches worldwide, located mainly in the US, as well as in the UK, Canada, China, Denmark, Germany, India, Israel, and Sweden.

Everyone is now asking: Will the collapse of SVB lead to a greater systemic failure? Who will now acquire the SVB business, its assets, its intangible assets including its technology and its premium brand?

Silicon Valley Bank, which was headquartered in Santa Clara, California, was the bank of choice for many entrepreneurs, startups, growth companies, and investors (including venture capital funds) in the innovation and technology-led economy. SVB, well-known as a Tech Lender, held approximately US$209 billion in assets as of early March 2023. SVB had a significant rise in deposits over the last few years.

Over a period of just 48 hours at the end of last week, SVB was hit by a capital crisis and a bank run, as well as with rapidly raising interest rates implemented recently by the US Federal Reserve (the Fed). SVB was shut down by US regulators on Friday.

By the end of Thursday of last week and over the period of a single day, customers had suddenly withdrawn over US$42 billion of deposits from SVB, a quarter of its total deposits, according to the Financial Times (FT, article entitled “Silicon Valley Bank shut down by US banking regulators”). SVB has failed to raise new capital to counter the outflows of deposits.

The Financial Times reported that the Federal Deposit Insurance Corporation (FDIC) insures only deposits up to US$250k, and approximately 96% of SVB's deposits, which amount to US$173 billion, were either uninsured or exceeded the insured limit. Most of SVB’s clients, however, mainly technology-led companies, had deposits significantly higher than this insured amount, in some instances in the hundreds of millions of dollars, as was the case with Roku, which had deposits in excess of US$480 million, (most of it uninsured), at the time SVB collapsed.

Over the last ten years, technology-led and VC-backed companies have been fuelled by low interest rates, which have led to cheap capital available for companies and more risk taking, assisting in the growth of starts-ups and growth companies. Many Venture and Growth Investors and their portfolio companies held deposits at SVB.

As a brief review on how banks operate, depositors place money into the bank, and these deposits now become a liability for the bank that it needs to repay, when the depositors withdraw the deposited funds. With this capital that has been deposited, the bank then lends out or makes investments (loans & investments) to try to capture a spread, which is essentially the return on the loans and investments made in excess to the amounts of the deposits. As long as the loans and investments exceed the value of the deposits, the bank will have a positive equity position.

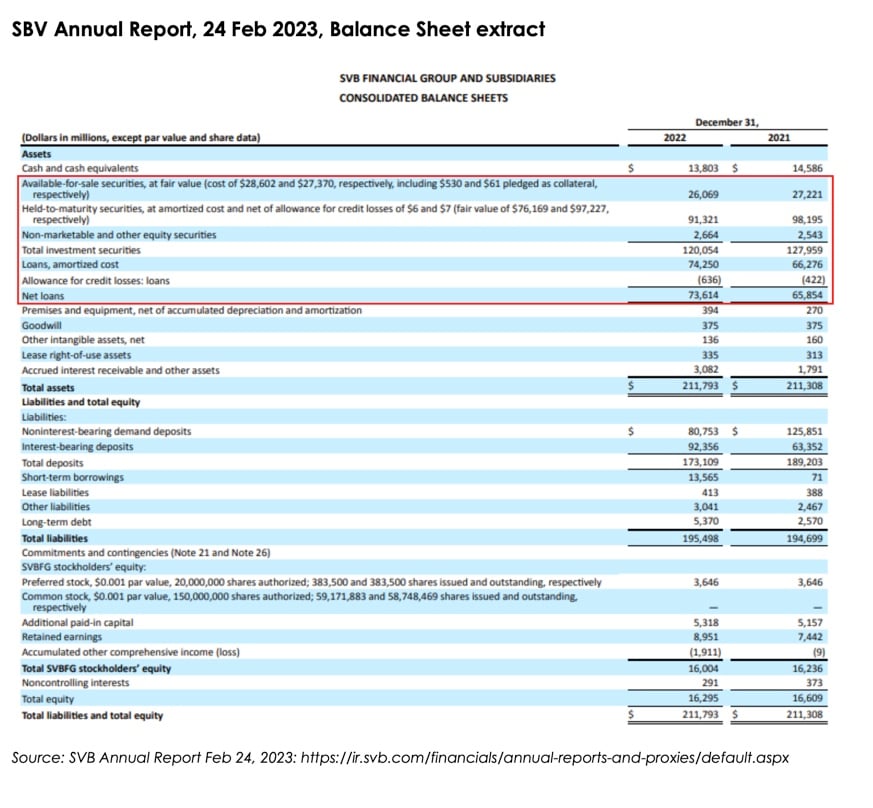

Banks typically have a regulatory requirement to maintain capital reserves as a safeguard against potential insolvency resulting from the withdrawal of deposits, as was the case with SVB. To properly analyse SVB's case, it is important to examine its current financial position, particularly the loans and investments section (please see extract below from its recent Annual Report). The balance sheet shows that SVB has (1) Investments in Available-for-Safe Securities (i.e., investments available for sale); (2) Investments in Held-to-Maturity Securities; (3) Non-marketable and other equity securities; and (4) Loans. SVB’s balance sheet positions on its investments, along with market factors, are key elements that triggered SVB’s recent collapse. What is important for one to understand about (1)-(4) above, is that for the Available-for-Sale Securities, one marks the value of the underlying securities to market on a regular basis. However, for Held-to-Maturity Securities, they are not marked to market unless one of the securities held in maturity is sold, in which case the entire book value must be marked to market in the Held-to-Maturity Securities investment portfolio. Banks are generally incentivised to allocate resources to the Held-to-Maturity investment portfolio. Held-to-maturity securities are generally not marked to market, and therefore this may result in a bank not recognising losses.

According to the FT and other sources, the collapse of SVB is linked to its decision to place approximately US$91 billion of its deposits in long-dated securities such as US Treasuries and mortgage bonds. Initially, these investments were perceived as safe; however, as the Fed aggressively raised interest rates, to 4.75% from nearly 0.0% a year ago, as it tries to fight inflation in the US, SVB’s investments plummeted by around US$15 billion compared to their purchase value.

Estimates have shown that the SVB deposits have decreased from US$198 billion in early 2022 to US$173 billion by 31 December 2022. Meanwhile, the offsetting assets were about US$191 billion (US$26 billion for Available-for-Safe Securities; US$91 billion Held-to-Maturity Securities; and Loans US$74 billion = US$ 191 billion). Therefore, if one analyses the Balance Sheet, there was approximately US$12 billion in net Equity. The problem is that in the Held-in-Maturity Securities portfolio there was a huge unrealised loss, taking it down from US$91 billion to US$76 billion), and therefore the SVB was insolvent considering these factors. Considering these losses in the Held-to-Maturity Securities portfolio, SVB is actually in a negative Equity position. As soon as cash deposits were quickly withdrawn last week, led by investor and companies fears as they tried to access their capital, the bank collapsed.

The SVB crisis has significant implications for the technology industry, particularly for startups and venture capital firms. SVB's lending practices have been critical in providing capital to startups and fostering innovation. However, the crisis has highlighted the risks associated with such lending practices and the need for startups to manage their finances prudently.

I have spoken with several of my friends over this weekend who are CEOs and CFOs of US and UK based firms and funds, all who are very worried about the current situation. One CFO from a UK based Cambridge technology firm stated that it had payroll deposits in SVB, and therefore it had limited its potential losses due to SVB’s collapse. Other firms were not as fortunate.

The crisis has also raised concerns about the financial stability of other banks catering to the technology industry. Many financial institutions have entered the technology sector in recent years, attracted by its high growth potential. However, the SVB crisis has shown that the sector is not immune to economic shocks and that financial institutions need to exercise caution when lending to technology companies.

The Bank of England had put the UK arm of SVB into resolution, after SVB applied for £1.8 billion of liquidity. As of today 13 March, it was announced that HSBC acquired the UK arm of Silicon Valley Bank for £1, which brought great relief to UK based technology companies.

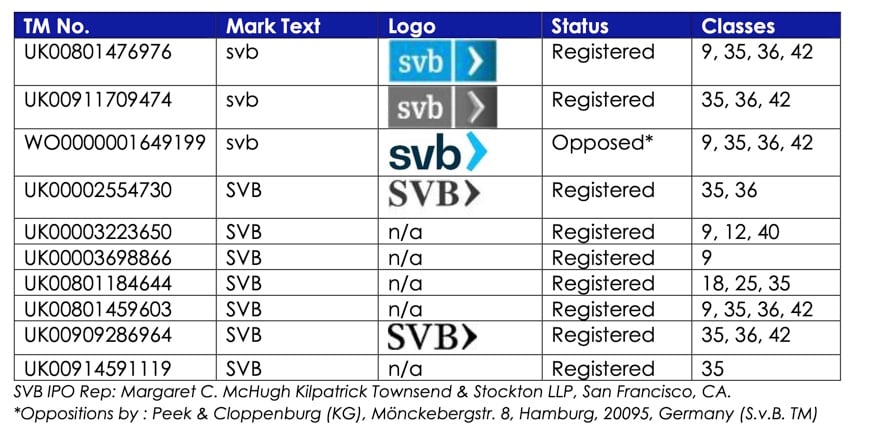

As part of SVB’s value, the company had a premium brand with several registered trademarks globally. In the UK, more specifically, SVB (under the ownership of its parent company: SVB Financial Group, located at 3005 Tasman Drive, Santa Clara, California, 95054, United States of America) had the following “SVB” registered (and opposed) trademarks in word format and logos below:

According to both short sellers and market analysts (such as William C. Martin), as reported by Bloomberg, the problems that led to SVB’s failure were visible in balancesheet figures of the firm’s most recent earnings report. Please see the Balance Sheet extract from the SBV Annual Report, 24 Feb 2023, below.

Analysts had observed that SVB had significantly increased its holdings of securities in the bond market over the recent years. They also noticed that the bank has become heavily exposed to fixed-income investments , following a year of significant losses in the bond market. Problems arise when a large portion of the bank's uninsured deposits is at risk, as was the case with SVB. These deposits constitute a significant part of the operational funds (cash), and are essentially in great part the operating case of many VCs and technology companies. Without this operating cash available, companies can collapse.

It will be interesting to see how this will ultimately affect private capital and VC- backed technology portfolio company valuations and investments around the world and VC, and PE sentiments overall, with increased market and company associated risk.

Jefferies CEO stated that a “merger occurring today” would be the best outcome for SVB, to resolve the failure of SVB, according to reports from Bloomberg.

The SVB crisis has been a wake-up call for the technology industry and the financial institutions catering to it. The crisis has highlighted the need for startups to manage their finances prudently, and for banks to exercise caution when lending within the bond market. We will be watching closely how markets and investors around the world react and adjust to tackle the current crisis at SVB and other similar financial institutions globally.

Send us your thoughts: